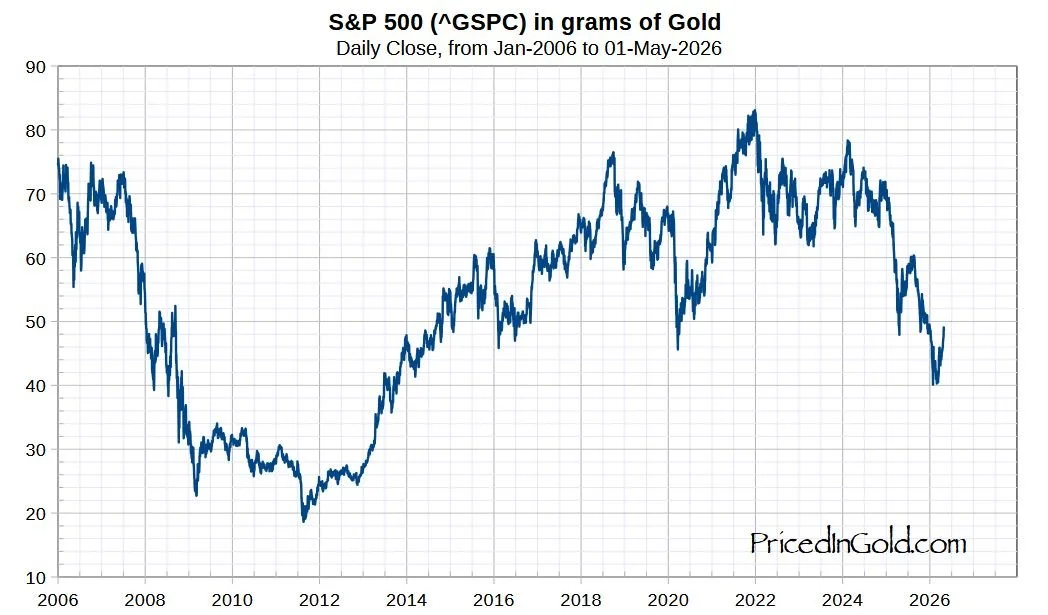

s&p 500 in gold

The way we measure investment performance shapes the conclusions we draw. Most investors evaluate success in nominal terms—how much their portfolio has grown in dollars. But dollars are not a stable unit of value. They are influenced by inflation, monetary policy, and broader economic forces. When we change the measuring stick, the story changes. Pricing equities in gold—an enduring store of value—offers a clearer view of real wealth.

Looking at the S&P 500 priced in gold from 2006 to today tells a different story than traditional charts. From 2006 to around 2011, equities lost nearly 70% of their value relative to gold. This reflected not just falling stock prices, but a flight to hard assets during a period of crisis and monetary intervention. From 2011 through 2022, equities strongly outperformed as liquidity and low rates fueled financial assets. Since 2022, however, equities have again declined in gold terms, signaling a shift in underlying dynamics.

This highlights a key truth: returns depend heavily on the macro regime. A portfolio can rise in dollar terms while losing real purchasing power. Yet most portfolios remain heavily concentrated in equities and bonds, implicitly betting on continued financial asset dominance. That is not true diversification—it is reliance on a specific economic environment.

Today’s backdrop suggests that environment may be changing. Higher debt levels, persistent inflation pressures, and geopolitical fragmentation point to greater uncertainty. In such regimes, gold and other real assets are not “alternatives”—they are essential components of preserving wealth.

Institutional portfolios reflect this reality. They diversify across multiple return drivers—equities, duration, real assets, and alternatives—rather than relying on a single source of performance. The goal is not just to maximize returns, but to maintain resilience across cycles.

Ultimately, wealth is defined by purchasing power, not nominal gains. Measuring performance only in dollars can obscure risk. Evaluating it in real terms reveals whether a portfolio is truly compounding value or simply tracking a declining currency. A portfolio that can lose 30–50% relative to real assets is taking more risk than it appears—and that risk often only becomes visible when the regime shifts.

the traditional 60/40 portfolio (60% stocks / 40% bonds)

For decades, the traditional 60/40 portfolio (60% stocks / 40% bonds) was considered the gold standard for long-term investing.

And to be fair, it worked well during a very specific era:

• Falling interest rates

• Low inflation

• Globalization

• Expanding valuations

• Strong bond diversification

But many affluent investors are starting to ask a difficult question:

What if the environment that made the 60/40 model successful no longer exists?

Modern markets are becoming increasingly concentrated, correlated, and policy-driven.

Today:

• U.S. equity valuations remain historically elevated

• Government debt continues rising

• Inflation has become more volatile

• Bonds still carry meaningful duration risk

• A handful of mega-cap tech stocks increasingly drive index returns

This creates a challenge many investors don’t fully appreciate:

A traditional portfolio may appear diversified on paper while still depending on a narrow set of economic outcomes.

In many cases, both stocks and bonds rely on:

• Stable disinflation

• Continued liquidity expansion

• Central bank intervention

• Healthy economic growth

When those assumptions break down, diversification can fail exactly when investors need it most.

We saw glimpses of this in 2022:

Stocks fell.

Bonds fell.

Traditional diversification struggled.

That forced many affluent families, business owners, and retirees to reconsider whether the conventional approach is truly built for long-term resilience.

Increasingly, sophisticated investors are exploring broader portfolio approaches that may include:

• Precious metals

• Real estate and REITs

• Alternative strategies

• Private credit

• Managed futures

• Global diversification

• Inflation-sensitive assets

• Selective commodity exposure

The objective is not to “predict the future.”

It’s to reduce dependence on any single economic regime.

Because real wealth preservation is not just about maximizing returns during favorable periods.

It’s about maintaining purchasing power, managing risk, and staying resilient across multiple environments:

• Inflation

• Deflation

• Recession

• Stagflation

• Currency debasement

• Liquidity crises

This becomes even more important near retirement, where sequence-of-return risk can permanently alter outcomes after large drawdowns.

At Analog Capital Partners, we believe thoughtful diversification should extend beyond simply splitting capital between stocks and bonds.

We focus on globally diversified, multi-asset portfolios designed to navigate a wider range of economic conditions while aligning with each client’s long-term goals, liquidity needs, and risk tolerance.

The investing landscape is evolving.

Many affluent investors are evolving with it.